Tag: Christie’s

-

Putting the hammer on the Big 2 good for collectors

This article was first published March 5th, 2000, in the Sunday Business Post The number of column inches that the price-fixing fiasco between Sotheby’s and Christie’s has received recently has been nothing short of startling. But the subsequent resignations, the US Justice Department antitrust investigations and the outcry from clients and shareholders have to a…

-

Auction Houses go online

This article was first published April 2, 2000 in the Sunday Business Post. Auction Houses go Online They said it couldn’t last. For months the analysts have been painting the walls with a dark thick impasto. The message was there for all to see – internet stocks were simply selling way above their value. As…

-

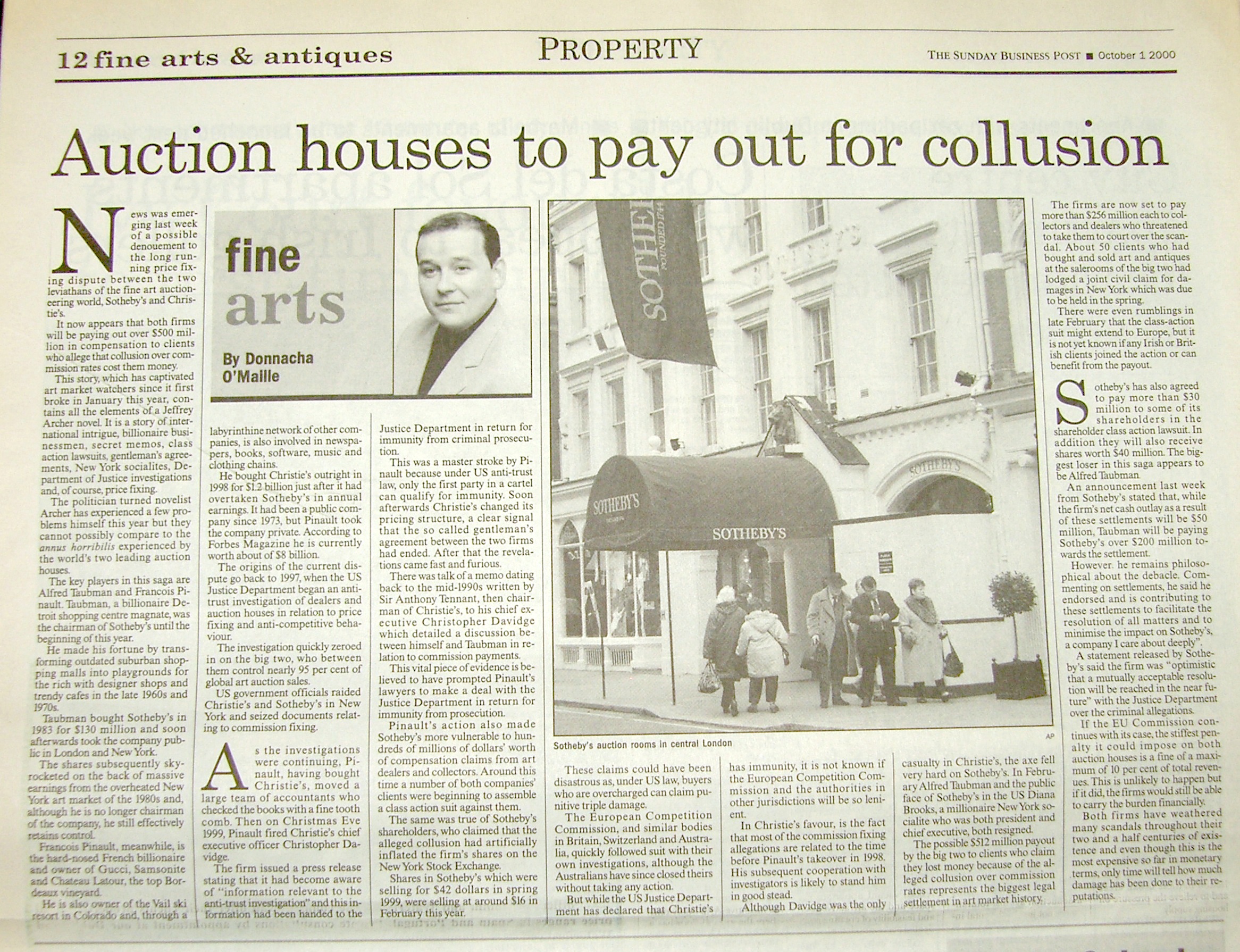

Auction houses to pay for collusion

This article was first published in the Sunday Business Post, October 1st 2000 News was emerging last week of a possible denouement to the long running price fixing dispute between the two leviathans of the fine art auctioneering world, Sotheby’s and Christie’s It now appears that both firms will be paying out over $500 million…